Why Do You Think You're Prepared to Discuss Long-Term Care?

If someone from the advisory community actually engages the typical American consumer about LTC Planning, the conversation almost always starts with the words ‘nursing home’ and predicates the discussion on fear rather than fundamentals. The reality is very different: according to the American Association for Long-Term Care Insurance, 71% of claims start with home care, 13% begin in assisted living, and only 16% begin in a nursing home. Which means the conversation must start with a ‘plan for’ discussion — and that requires an advisor to actually understand how and where care is delivered.

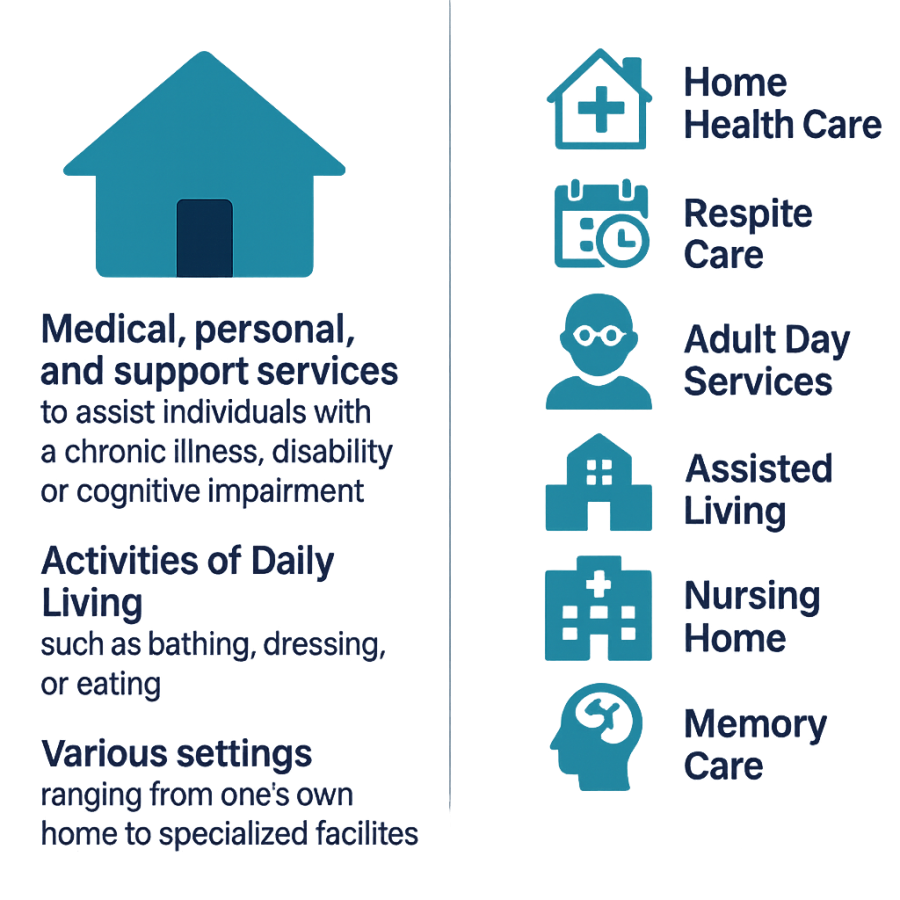

Furthermore, nursing homes are not only the least likely setting where care begins — they’re also the one most consumers want to avoid at all costs. In fact, AARP research shows that 77% of adults age 50 and older want to remain in their homes as they age, a number that has stayed consistent for more than a decade. That’s why the conversation must shift to the broader range of real care options: Home Health Care, Adult Day Services, Assisted Living, and Memory Care. Only then can clients plan with the clarity, confidence, and relevance they deserve.

What is Long-Term Care?

Sometimes it helps to take a step back and define what we’re really talking about. Long-Term Care (LTC) refers to a range of medical, personal, and support services designed to assist individuals who have a chronic illness, disability, or cognitive impairment and can no longer perform some or all of the Activities of Daily Living (ADLs), such as bathing, dressing, or eating. These services may be provided in various settings — from the comfort of one’s home to assisted living, memory care, or skilled nursing facilities. The real disconnect for the advisory community isn’t in defining LTC — it’s in understanding what actually happens next in the care management process

Earlier this summer, I asked a serious question: “What Gives You The Right To Talk About Long-Term Care?” The context then was competency — how does one’s core expertise actually qualify them to have this conversation? Let’s press further with a few blunt examples:

-

How does understanding asset allocation educate you about Hospice? It doesn’t.

-

How does drafting a trust allow you to differentiate levels of home healthcare? It doesn’t.

-

How does preparing a tax return give you insight into memory care? It doesn’t.

And yet, here we are. Seventy-five million Baby Boomers are heading into and through retirement, while the advisory community — ill-equipped at best — continues to dispense LTC Planning recommendations as if spreadsheets, legal documents, or tax codes alone solve the problem.

Maximizing Long-Term Care Engagements

To help clients truly understand the full spectrum of services that support chronic illness, disability, or ADL impairments — and actually plan for it — advisors must change their behavior. That means:

-

Meeting with Home Health Care providers and touring facilities to see what real care looks like.

-

Dispelling myths about what Medicare and Medicaid do — and don’t — cover.

-

Clarifying care preferences and expectations before a crisis hits.

-

Encouraging earlier, more intentional planning instead of deferring uncomfortable conversations.

To that end, a well-designed LTC Plan should:

-

Be comprehensive, structured, and in writing

-

Address coverage across the full care continuum

-

Incorporate a tax and legal framework that supports the plan

-

Be integrated with the client’s risk management, financial, estate, and retirement strategies

-

Recognize that self-funding is not a plan — it’s the default, and it rarely works

If you feel ‘qualified’ to help clients navigate the LTC Planning process after reading this, you’re not. But by all means, keep doing what you’re doing — if your goal is to be replaced by AI, TurboTax, Trust & Will, or Vanguard’s robo-advisor. Or, perhaps you can embrace the reality that LTC Planning is “inconvenient” because it forces you to step up and expand beyond your comfort zone, admit limitations, and collaborate. Maybe LTC Planning pushes you out of the way, with the acknowledgement you're not equipped for it, or you pretend you are.

While every client isn’t a candidate for an insurance-based LTC plan, far too many are dissuaded by someone who can’t even legally sell insurance. Therein lies the hypocrisy. Every professional in the advisory community is licensed for what they do — attorneys for the practice of law, EAs or CPAs for tax work, advisors for investments. And every one of them knows they can’t operate outside the scope of that license. Yet, somehow, when it comes to Long-Term Care Planning — both the topic itself and the qualifications required to engage — those standards get ignored.

Clients deserve and expect their advisors to do the job they’re paid for, but they don’t expect the Medicare agent to manage their asset allocation, the estate planning attorney to design a retirement income strategy, or the financial planner to draft a trust. So why do some think it’s acceptable to play in another sandbox when they don’t hold the license to do so? No license, no credibility. Anything else is malpractice disguised as advice.

The least you can do, if you’re going to step into the LTC Planning space, is know the basics. And after starting INERTIA in 2011, I can confidently say you have MUCH to learn. If you’re unwilling or unable to accept that, you’re not planning — you’re pretending. And your clients will pay the price for your actions.

20250927