Charlie & Carol Cash: RMDs & Long-Term Care Planning

Most families don’t avoid Long-Term Care Planning because they don’t care; they avoid it because they don’t know how to connect it to the rest of the financial plan. However, proactive planning across generations leads to better long-term decisions. In this case study, we make the following planning assumptions:

-

The couple, both 70 years old, are quite active & healthy.

-

Pension and Social Security fully cover their income needs.

-

They want to avoid becoming a burden on their children/grandchildren.

-

They would “pay for care” with untapped $600,000 in retirement accounts.

-

Carol also sees those accounts as "legacy assets" to pass on what they don't use to their children/grandchildren.

-

The couple must begin taking Required Minimum Distributions (RMD) soon.

-

Their CPA indicates annual RMDs is excess of $22,000.

-

They complete CARE Profiles projecting a combined future care need of 6-years, at $7,500/month.

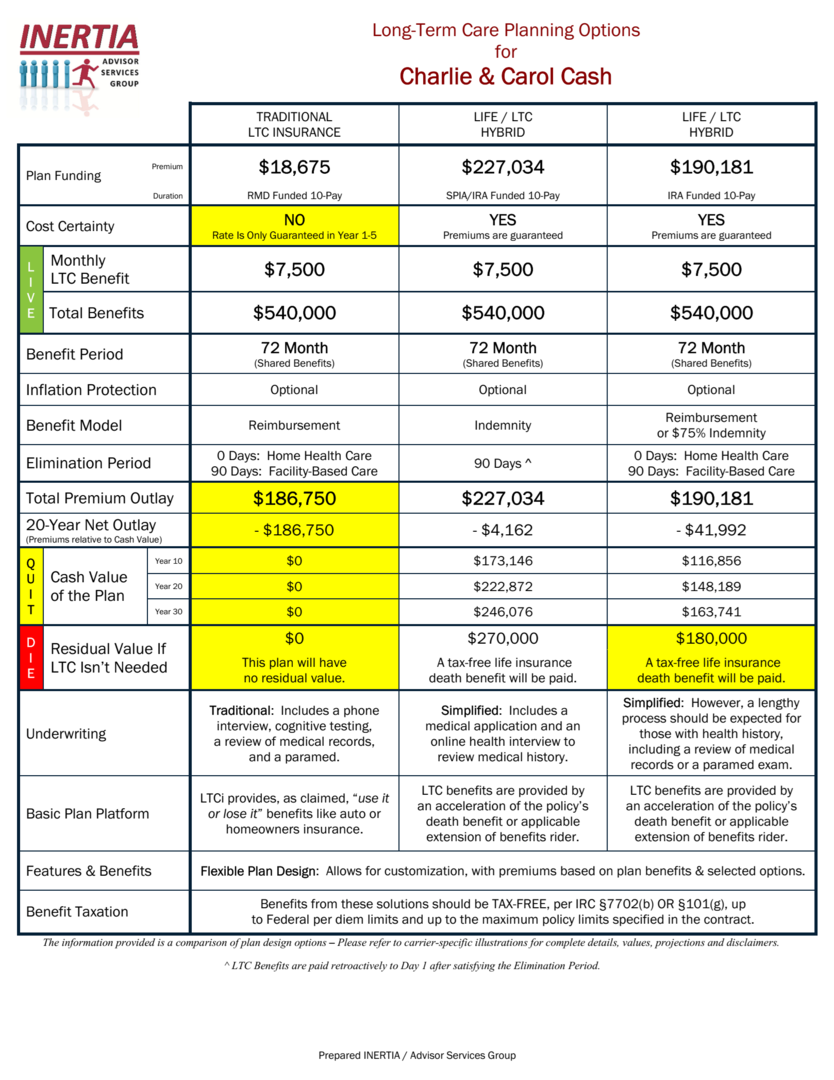

Without a formal funding plan for future care needs, those RMDs will simply flow through the tax system each year—creating taxable income while the underlying Long-Term Care risk remains fully exposed.

Unspoken, however, is the couple's reality: their “legacy” assets are already allocated to an off-balance-sheet, unaccounted-for Long-Term Care risk—whether they know it or not. When that risk becomes a care event, optionality is lost, as those assets must be used to cover a liability that suddenly hits the income statement.

Which of these options would you recommend to Charlie and Carol to efficiently reposition their RMDs to address Long-Term Care risk while preserving legacy assets?

And....Does your current LTC wholesaling resource provide a presentation tool like this?

Age 72 may not be the optimum age to set up a Long-Term Care Plan, but funding the plan with qualified funds can provide substantial benefits and minimize the impact of age affecting the plan.

230807