Sam & Sue Banks: Long-Term Care Planning And The Look-Alike Roth IRA

Long-Term Care (LTC) is one of the most predictable yet least planned for financial risks facing Americans in or near retirement, especially for the affluent. For many, the issue isn’t whether they can afford care. It’s how that risk is funded, structured, and integrated into the broader financial and estate plan. With that in mind, consider the "Look-Alike Roth IRA" strategy as an effective way to introduce Long-Term Care Planning—particularly for high-net-worth clients seeking tax-efficient outcomes.

The “Look-Alike Roth IRA” doesn’t replicate a Roth IRA—but it creates Roth-like tax outcomes while addressing one of the most overlooked risks in planning: Long-Term Care. By repositioning assets into an asset-based (“hybrid”) LTC solution, the strategy is designed to fund a known future liability while providing features that affluent clients typically associate with Roth-style planning:

- No income caps or contribution limits

- TAX-FREE distributions when used for Long-Term Care.

- Defined funding with cost certainty - Both the amount and duration can be structured in advance.

- Removes Long-Term Care risk from the broader investment and income plan.

- Reduces reliance on a spouse or loved ones as default caregivers or care managers.

- Prevents untimely or forced liquidation of portfolio assets during a care event.

- Flexibility and control through a "Live, Quit, or Die" framework.

- Estate efficiency with a TAX-FREE death benefit if care is not needed.

- Provides a dedicated “pay for” account designed to avoid triggering Medicare premium surcharges (IRMAA)

- Protects legacy assets by transferring Long-Term Care risk away from the estate.

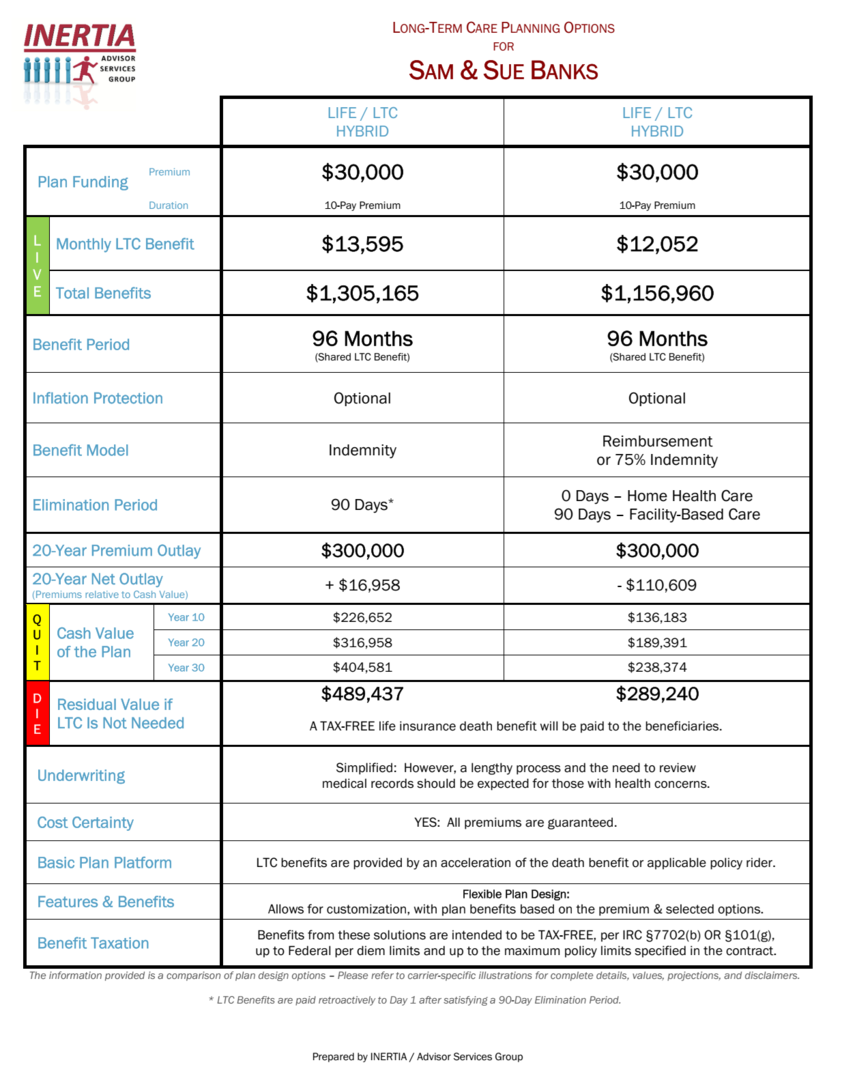

While the Look-Alike Roth IRA may not suit every client, the case study below introduces the concept and shows how it can be incorporated into planning discussions.....

- Sam & Sue are both 60 years old.

- They have approximately $7M in assets in non-qualified and qualified accounts.

- Their CPA advised against a Roth IRA conversion, even though they like the concept.

- Their income exceeds the limits for Roth IRA eligibility.

- Their individual CARE Profiles project a total eight-year need for care.

- Their current Long-Term Care "plan" would be to self-fund the cost of care.

- Contributions of $30,000/year for 10 years ($300,000) into a Look-Alike Roth IRA LTC Plan are appealing because they provide the couple with:

1) A TAX-FREE pool of funds to pay for care or.....

2) A TAX-FREE death benefit for heirs if care is not required, and.....

3) Control over the funding strategy.

How many of your affluent clients could appreciate this strategy for their estate and financial planning?

And....Does your current LTC wholesaling resource provide a presentation tool like this?