Sally Saver: When Can I Stop Paying for My Plan?

Long-Term Care (LTC) planning isn’t just about solving for the risk - it’s about doing so with a finite commitment over a defined period of time. So, whether the client believes they have sufficient assets to pay for future care - or they prefer to fund a plan over time - the real question becomes how to align their resources to effectively mitigate the Long-Term Care risk.

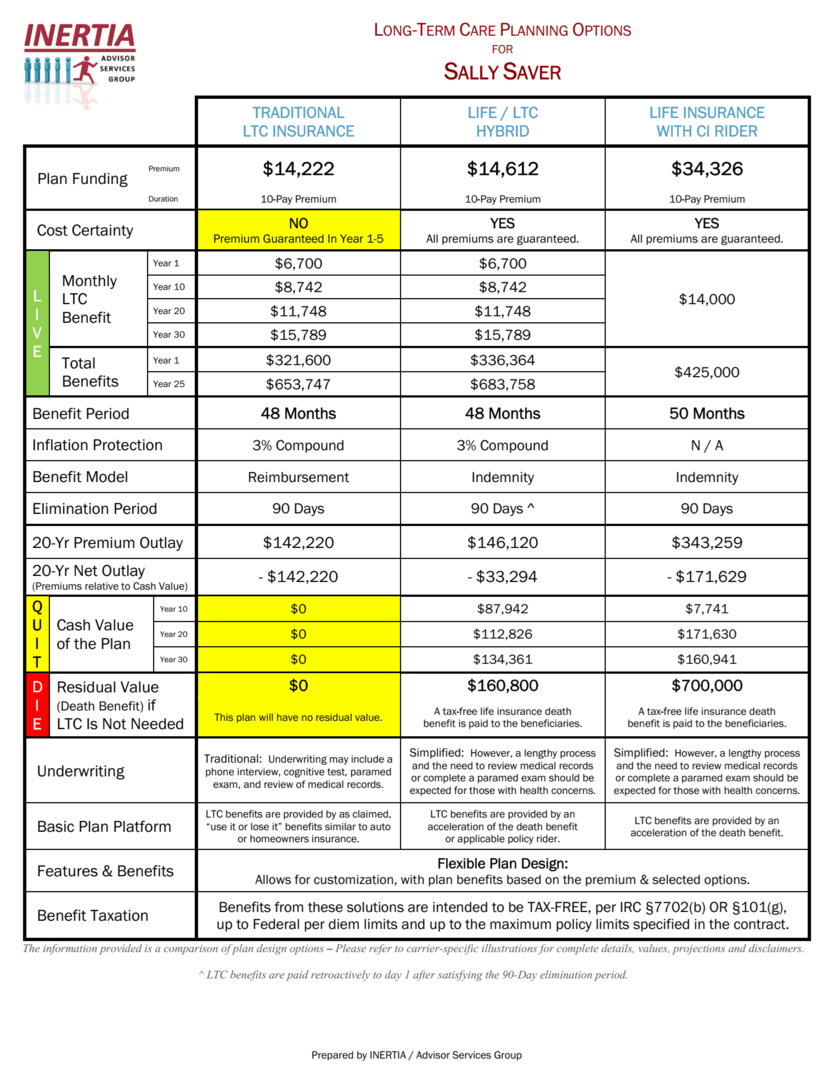

In this case study, we make the following planning assumptions:

- Sally is 60 years old and recently divorced.

- She has approximately $500,000 in assets, primarily home equity, in lieu of a portion of her ex-husband’s retirement accounts.

- She will receive $5,000/month in alimony from her ex-husband until age 70, when she can elect her maximum Social Security benefit. The alimony will far exceed what’s necessary to maintain her lifestyle.

- Her current Long-Term Care “plan” is to rely on that alimony over the next 10 years, but she is uncertain about accessing home equity beyond that period.

-

Her CARE Profile projects a four-year care need with a current cost of care at $6,700 per month.

This creates a fundamental mismatch: temporary income and retirement assets being relied upon to fund a risk that is both permanent and unpredictable.

If Sally were your client, which of the LTC Planning solutions would you recommend to maximize her funding sources and address her comprehensive planning goals?

And....Does your current LTC wholesaling resource provide a presentation tool like this?