Nick & Nancy Newlywed: The Power of the Pension Protection Act

Long-Term Care (LTC) Planning for couples introduces unique variables, especially for those in a second marriage. Without proper planning, one spouse is highly likely to become a caregiver and/or outlive the other after a care event. At the same time, blended family dynamics often create competing priorities around how assets are ultimately distributed. That combination — care risk + legacy intent — is where most plans break down.

For this case study, we make the following planning assumptions:

- Nick & Nancy, both are age 65

- Recently married (Second marriage for each)

- Both have assets and plan to retire this year.

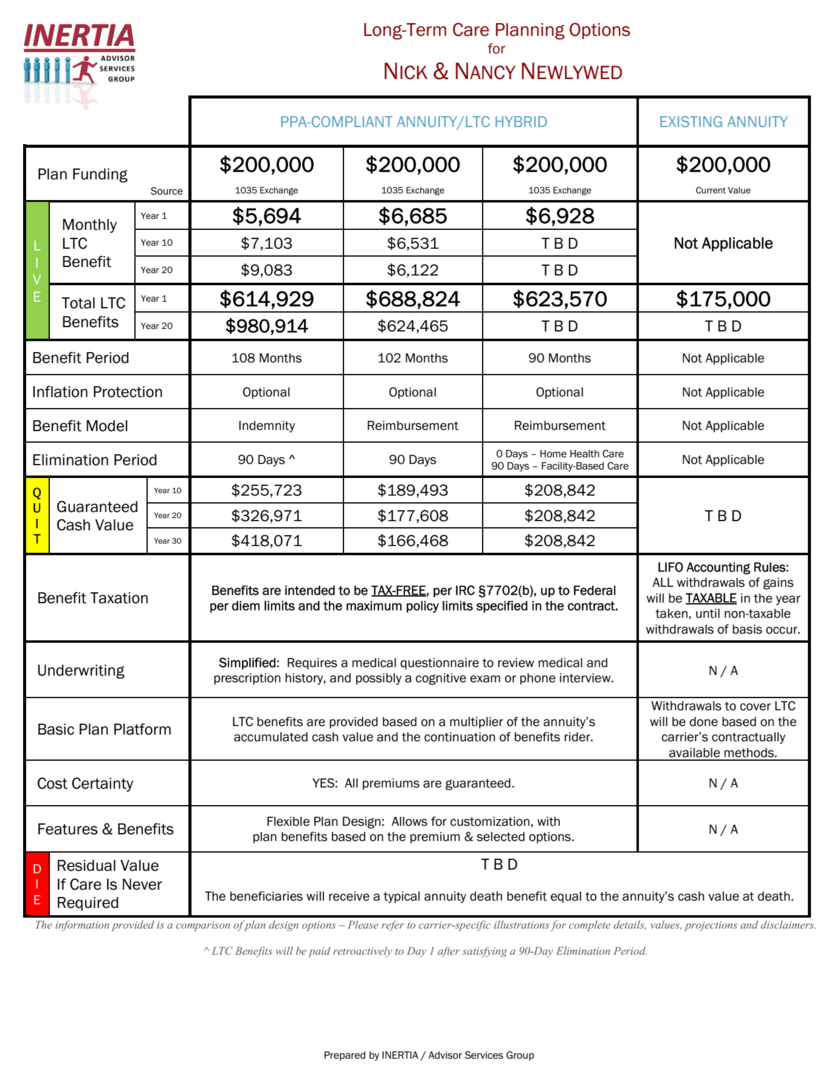

- They would “pay for care” with $200,000 in Nancy's existing annuity, which has a $100,000 Cost Basis.

- Concerned about becoming a burden on one another and their families.

- They were unaware of the Pension Protection Act (PPA) and how to leverage it and turn Nancy's single-life annuity into a joint-life LTC Plan.

The Planning Goal: How do Nick & Nancy avoid becoming caregivers for one another, preserve flexibility for the surviving spouse, respect legacy intentions for separate heirs, and maximize an existing asset beyond the default?

Which option below achieves their LTC planning goal by maximizing the existing annuity?

And....Does your current LTC wholesaling resource provide a presentation tool like this?

By planning ahead, your clients can upgrade an existing annuity (1035 Exchange) to a PPA-compliant LTC Annuity TAX-FREE and then, when necessary, take TAX-FREE withdrawals from the new annuity to cover qualifying Long-Term Care expenses in the future. All with ZERO out-of-pocket cost!

230807