Betty Boomer: The Risk-Averse Retired Widow & Grandma

Healthcare In Retirement and Long-Term Care (LTC) are not "important topics" for women; they are defined financial exposures that are usually ignored. For those like Betty, the risk is not theoretical but measurable and already present. In this case study, we make the following planning assumptions:

- She has social security and pension income to maintain her lifestyle.

- Betty is 65 years old and has $750,000 in assets

- $165,000 in growth-oriented mutual funds.

- $160,000 in a non-spousal beneficiary IRA, she recently received.

- $225,000 in an existing fixed annuity, with a $75,000 cost-basis

- $200,000 in low-risk, low-yield deposit accounts.

- On paper, Betty appears “low risk” but in reality, she is carrying a concentrated, undefined healthcare liability against those assets.

- Her Long-Term Care "plan" would be to tap the deposit accounts - assets intended for a "legacy" that would pass to her family - without defining how or when the funds will be accessed, or what happens if the liability exceeds them.

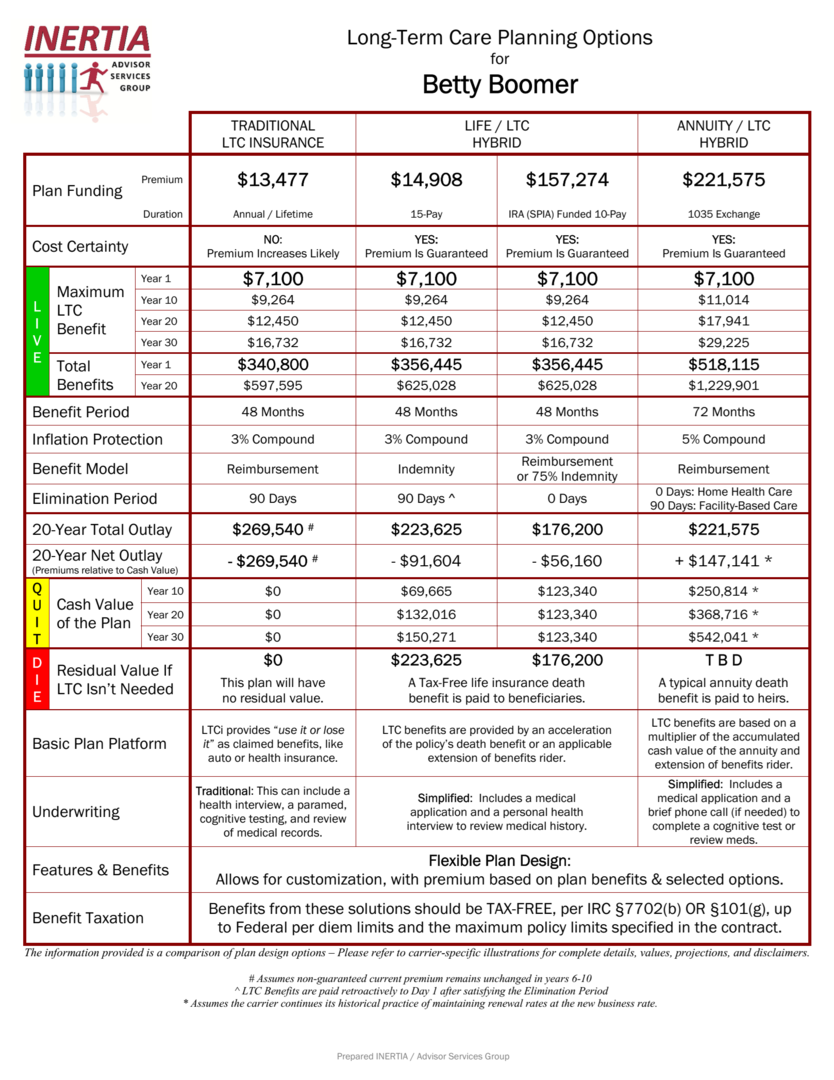

- Her CARE Profile projects a four-year, $7,100/month, inflation-adjusted future care need, creating a $340,000 unfunded liability - Before taxes, market volatility, or timing are considered.

If Betty were your client, how would this liability be measured, monitored, and mitigated within the plan to maximize her funding sources and address her comprehensive financial planning goals?

Does your current LTC wholesaling resource help you define the liability this clearly—or just quote around it?