Market Volatility Makes The Case for Long-Term Care Planning

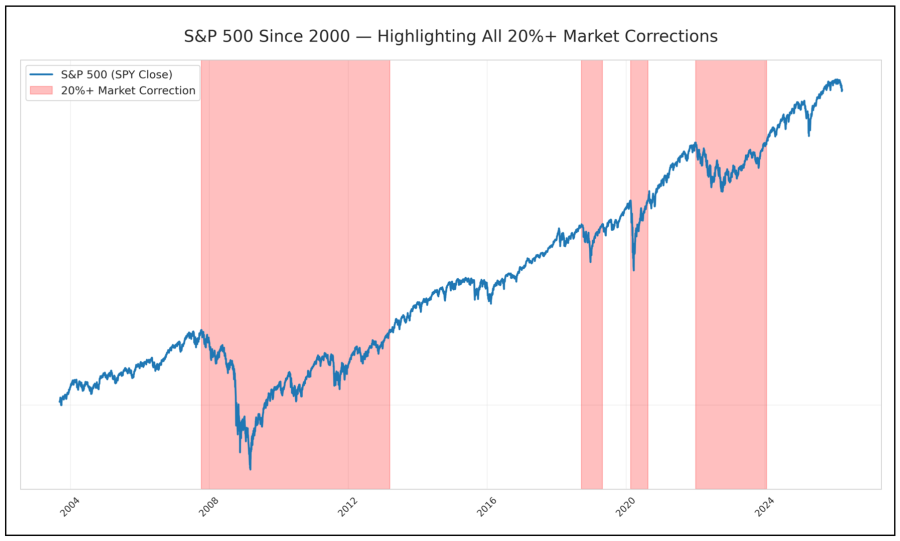

Here’s a challenge for those of you in the advisory community…..What is the significance of the following dates?

March 2000 - October 2002

October 2007 - March 2009

August 2011

December 2018

February - March 2020

January 2002 - January 2024

Now ask most Americans to identify the significance of those dates—some of the most severe market corrections in the past 30 years—and most couldn’t tell you. Because those events, and the fear they created in the moment, were temporary. The markets recover, and life goes on, yet every time volatility returns, the same panic follows.

Advisors step in, reminding clients to stay the course—and they’re right. Over time, markets recover. But here’s the question almost no one asks: What happens when the market doesn’t have time to recover? What happens when the market is down—and a Long-Term Care event shows up anyway? Because when it does, there is no recovery—only reaction. Ask those same Americans (your clients) to recall a moment when their health, or the health of a loved one, drastically changed. That date is unforgettable.

The Real Risk Is Not Market Volatility

Advisors and clients alike often become anxious over temporary events that resolve themselves. While markets fall and markets recover, the real danger isn’t volatility itself but the fixation on it. Meanwhile, there are more significant risks growing quietly in the background, and one of those is the need for Long-Term Care. Where market corrections resolve themselves, the need for LTC usually won’t have a resolution, as it often becomes chronic/permanent, and ignoring the topic won’t make the risk go away.

Pragmatically, if the market is down when the need for care arrives, the plan doesn’t recover—it breaks.

The Reality of Market Corrections vs. LTC Needs

The financial industry trains clients to believe that market movement is the greatest threat to their financial plans, but the irony is they prepare for the temporary and ignore the inevitable. Long-Term Care risk doesn’t correct itself. It only grows more urgent with time. Financial Planning — and the Long-Term Care component — isn’t about timing the market. It’s about preparing for risks in life that won’t or can’t self-correct.

Why Insurance-Based LTC Planning Makes Sense

An insurance-based Long-Term Care plan removes the market from the equation entirely because the issue isn’t volatility; it’s timing.

Market Volatility Becomes Irrelevant: When care is needed, benefits are available regardless of what the market is doing. There is no dependence on recovery, no waiting, and no sequencing risk.

No Forced Liquidations: Without a defined funding source, care is funded by selling assets — often when markets are down. That locks in losses, accelerates depletion, and leads to unnecessary tax consequences. An insurance-based plan avoids that entirely.

Tax Efficiency Is Built In: LTC benefits are received income tax-free, preserving assets that would otherwise be reduced by taxes if liquidated to pay for care.

Funding Becomes Defined, Not Assumed: Recurring premiums function as a deliberate funding strategy — like Dollar Cost Averaging — but instead of accumulating assets, they transfer risk. The outcome is known. The exposure is not left to chance.

The bottom line is this: If Long-Term Care risk isn’t addressed in a financial plan, then the plan is incomplete. And if that plan depends on market performance to fund a care event, then it's an assumption and not a strategy. The real question isn’t whether the conversation happens, but how it’s framed in a way that leads to action — Before the market or life forces the decision.

20260324