Managing The "Risks of Aging"

The pandemic provided a glimpse into what a "stressed" American healthcare system might look like; however, with a "Silver Tsunami" approaching, when 1 in 5 Americans will be over age 65, that stress test may have been just the warm-up act before the main event.....

Surveys indicate that many Americans approaching retirement don't fully comprehend the financial risks associated with healthcare in retirement and Long-Term Care (LTC)1. This lack of awareness can lead to inadequate financial planning, leaving retirees vulnerable to high medical costs that could potentially deplete their savings. Fidelity estimates1 that a couple retiring in 2025 will need $345,000 to cover significant healthcare expenses in retirement, including premiums, copays, deductibles, prescription drugs, etc., and their figures exclude the potential cost of LTC.

Underestimating these costs can significantly impact one's financial well-being during retirement. As this New York Times headline from 2019 indicates, "Many Americans Will Need Long-Term Care. Most won't be Able to Afford It." — The statement was true then, and it's just as accurate today…. only now with a kicker! According to TIAA2, only 14% of people age 60 and over have private long-term care insurance. In other words, the overwhelming majority are walking into retirement without a strategy to handle one of the most significant and most uncertain risks they face.

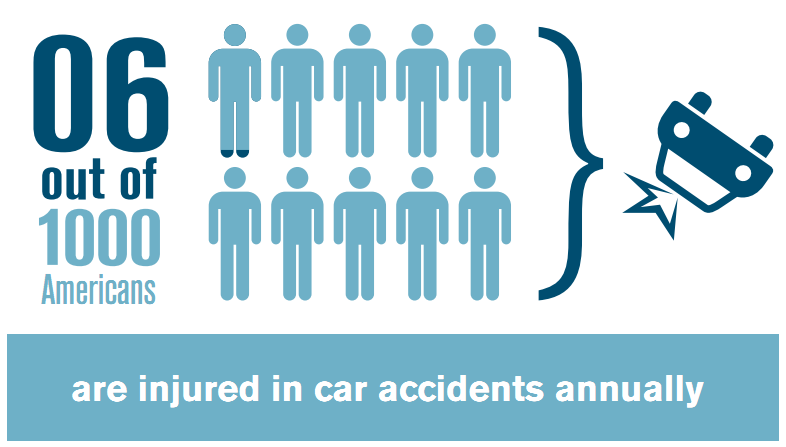

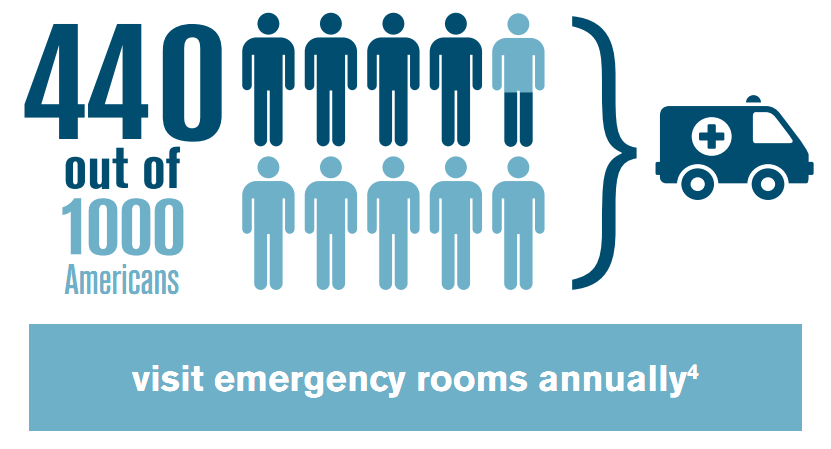

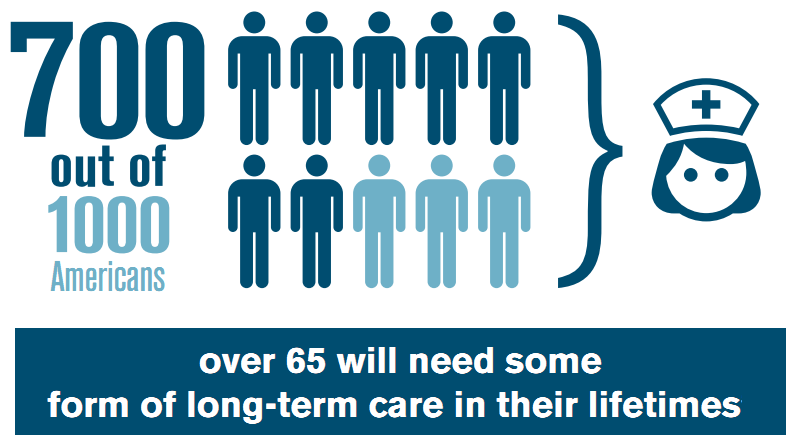

What the article really underscores—and what most Americans miss—is that LTC Planning isn't just about paying bills. It's about managing the Risks of Aging from a higher-level risk management perspective, and regardless of the advisory role with clients, it's imperative to use the tools at your disposal to quantify the potential impact of LTC on a family's finances in the context of that advisory relationship. For clients in or approaching retirement, recognizing these risks isn't optional—it's essential. (The graphics below highlight this further.)

Unfortunately, the financial risk of aging doesn’t stop with your clients. It can extend directly to their children through filial responsibility laws—statutes still on the books in 29 states.

What this means: These laws can impose a legal duty on adult children to cover the cost of care for indigent parents. They trace back to the Elizabethan Poor Law of 1601, and are rarely discussed in the advisory community.

Why it matters: Enforcement may be rare today, but it isn’t theoretical. The most recent cited example occurred in Pennsylvania, where John Pittas became responsible for nearly $93,000 of his mother’s care costs after an accident. One day, she simply walked out of the skilled nursing facility, moved to Greece with a boyfriend, and did so before qualifying for Medicaid. With no one else to pay her bills, the nursing home sued under Pennsylvania’s filial responsibility laws, and the court ruled her son was legally liable. For more details, click here to learn about John Pittas' case.

While the Pittas case may seem extreme, it highlights an uncomfortable truth: the risks of aging extend far beyond the individual. Families aren’t just vulnerable to high healthcare and LTC costs that can deplete retirement savings; they may also face direct financial liability under filial responsibility laws or the hidden costs of caregiving’s physical and emotional toll. Simply put, the “risk of aging” crosses generational lines.

With a Silver Tsunami approaching, the need for proactive planning for Healthcare In Retirement has never been greater. Whether it’s budgeting for the Fidelity estimate, moving the cost of long-term care from a footnote to a central planning component, or protecting loved ones from unforeseen liabilities, these are risk management conversations clients deserve to have initiated by their advisors.

Understanding the Risk of Aging may help clients see the need for Long-Term Care Planning.....

1 Fidelity Investments 2025 Retiree Health Care Cost Estimate, July 30, 2025

2 TIAA Institute, Misperceptions About Medicare, June 2025

20250902